2025 Trade: Geopolitical Realignment or Rerouting?

China rerouting its US-bound exports is being dressed up as geopolitical fragmentation.

By Richard Baldwin, Professor of International Economics, IMD Business School, Lausanne. 5 June 2026. Factful Friday.

Introduction.

2025 was the year geopolitical shocks should have fragmented world trade.

Washington started by weaponising its markets. Beijing responded by weaponising its supply chains.

McKinsey (2026) says 2025 trade showed an “emerging realignment of trade along geopolitical lines.” This updates the IMF (2025) description of the impact as “geoeconomic fragmentation along geopolitical lines.” UNCTAD (2026) says connector economies helped stabilise 2025 flows and cushion geopolitical fragmentation.[1]

But that’s not what really happened.

If we simplify to clarify: one cell in the world trade matrix collapsed; the cells around it rose.

It’s China rerouting its US-bound exports. I’m not denying that we are in the midst of World War Trade.[2] What I am denying is that trade is fragmenting. Fragmentation is a waffle word used to avoid pointing fingers and naming names in what is a much simpler reality.

So why do the serious studies keep finding fragmentation? Because, in my view, their metrics aren’t measuring what most readers think they are.

The subjects of today’s Factful Friday are the real impact on the 2025 trade pattern and shortcomings in the formal fragmentation metrics.

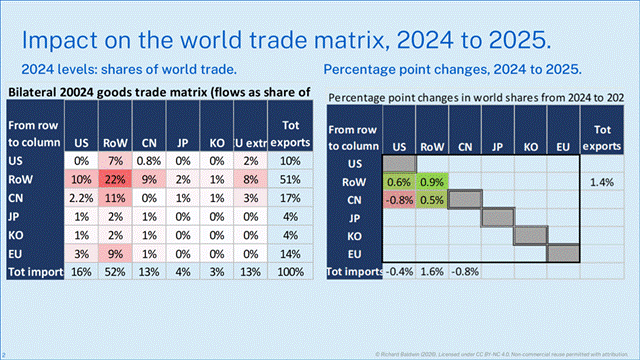

A really simple world trade matrix: Who exports to whom?

We have data on over 200 trading entities, so the whole from-to trade matrix has 200 rows and columns; that’s 40,000 entries. We need to simplify to clarify.

Conveniently, half of world trade is done by the US, China, EU, Japan, and Korea.

The trade matrix below shows these five plus a ‘rest of world (RoW)’ aggregate.[3]

The US, RoW and China are bunched together since that’s where all the 2025 action was.

[Chart: 2024 levels matrix and 2024–25 change matrix – reinsert from master]

As a warmup, the left table shows you the ‘before’ situation in 2024. Three key points to keep in mind when thinking about what fragmentation means at the world level.

1) RoW trade with itself is big, about a fifth of all trade.

2) US and China together account for about 25% of both imports and exports (see bottom row and rightmost column).

3) US-China bilateral trade is a small share of total world trade: US to China is 0.8% and China to US is 2.2%. Do the arithmetic: only 3% of world trade is directly affected by the bilateral trade war.

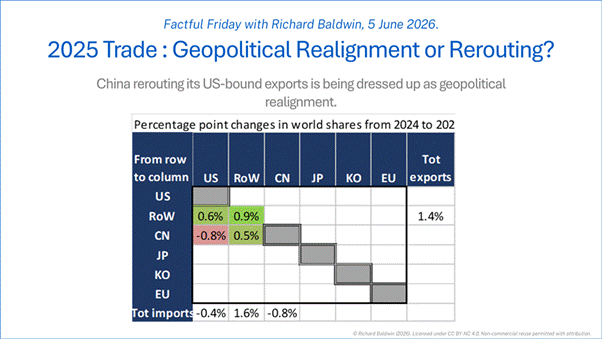

The headline fact.

The main chart in today’s Factful Friday column is on the right. It shows the percentage point changes in the bilateral flows between 2024 and 2025.

What should you look at first? The headline facts are all in the one red cell and two green ones next to it. Red signifies a drop; green a rise.

The red cell shows a drop of 0.8 percentage points in the China-to-US cell (first column, third row). Nothing shocking here; President Trump’s big, broad tariffs on China reduced Chinese exports to the US.

Or did they? The +0.6% number in the RoW to US cell and the +0.5% number in the China to RoW cell hint at a very simple story.

When US tariffs reduced imports from China, Chinese exports weren’t stymied; they were redirected. The US increased its imports from RoW by three-quarters of the China-US drop. And China increased its exports to RoW by just a tad less than the US increased imports from RoW.

The numbers don’t fit perfectly, but what do they suggest to you?

To me it looks like Chinese exporters found ways to circumvent the new US tariffs they faced. Not circumvention in the illegal sense, like tariff fraud, but rather commercial agility that made the best of a bad situation.

That’s why I think we should characterise the 2025 impact of World War Trade as “China rerouted its US-bound exports.” That is a lot less sinister than “world trade fragmented along geopolitical lines.”

“When I use a word, it means just what I choose it to mean,” Humpty Dumpty told Alice. And when the IMF say “fragmentation,” they are allowed to define it however they like. But would it be forward of me to suggest they are using a vague, politically neutral word to avoid naming countries and pointing fingers?

Be that as it may, we still have to understand why major studies keep finding ‘fragmentation along geopolitical lines.’ I’ll argue that these findings tell us more about the geopolitical proxies the studies use and less about geopolitical realities.

Viewing the world through bloc-tinted glasses.

The current best studies of the geopolitical impact on trade are advances on studies that were designed in a very different situation to today’s. This was the 2018 conflict between the US and China and its aftermath. Back then, the mainstream thinking was that the world, in the worst case, might break up into competing blocs. That is what happened in the 1930s.

The world has faced a very different shock since 2025. This isn’t a bilateral fight where nations might have to choose sides. It is an attack on all nations by the two biggest traders. In other words, none of the earlier frameworks were designed to evaluate the 2025 shock. And yet they were used for that.

The roaring publication success of the earlier studies led recent work to copy the basic set-up.

I’ll argue that the recent findings of geopolitical fragmentation reflect foundational assumptions from the earlier empirical literature rather than reality.

The key is the ‘monoculture’ of geopolitical proxies used to judge whether the world trade pattern is becoming more geopoliticised.

The 2025 shock changed trade patterns. To see if the result shifted the world towards geopolitical fragmentation, you have to have a measure of geopolitical alignment. The main one is based on the correlation of national voting in the UN General Assembly.[4] In theory, that seems a very sensible approach. It has been used in the political science literature, and it certainly worked during the Cold War when there really were competing trade blocs. Moreover, it avoids arbitrary, judgement-based allocations of countries to blocs.

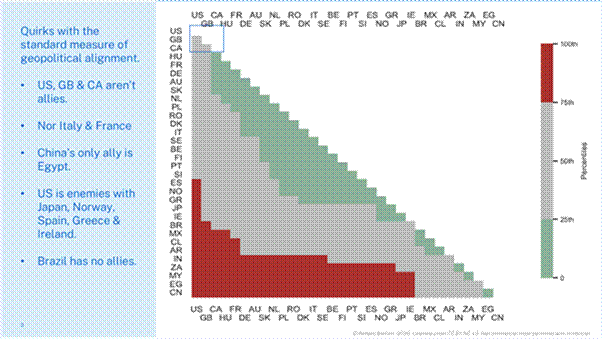

But in this case, the practice was quite different from the theory. An excellent BIS paper, “Deconstructing global trade: The role of geopolitical alignment,” unpacks it for us.[5]

Qiu et al (2024): “We rely on a distance metric proposed by Bailey et al (2017) that is often used in the literature as a proxy for geopolitical distance. Based on observed votes, they estimate a time-varying annual measure of each country’s political preferences, referred to as its “ideal point”. They then calculate the “geopolitical distance” between each pair of countries as the distance between their ideal points. (Graph 2). The larger the distance, the less aligned the two countries are.”

Nearly every headline study uses this, so it is worth having a closer look. The chart below, which is taken from Qiu et al (2024), shows some very strange results. Note that allies are shown by green cells, enemies by red cells, and ambiguous by grey cells. Here are some anomalies in the chart:

• The US, Britain, and Canada are not allies.

• Most of the allies in the chart are EU members and that makes sense since they can’t actually have different tariff policies as members of the EU customs union.

• But Italy and France are not allies, even though they’re both in the EU.

• China’s only ally is Egypt.

• The US is enemies with Japan, Norway, Spain, Ireland and Greece.

Impact on results.

Think about this for a minute. The 2025 shock decreased trade between the US and China. According to the proxy, that looks like geopolitical fragmentation (which of course it is). But the US is not allies with any of the RoW nations from whom it increased its imports in 2025. And China is not allies with the RoW nations it sent more exports to in 2025.

This one-hit, two-misses result blows a huge hole in the geopolitical fragmentation narrative, the bloc-based story that was so sensible in the last Trump-induced trade war.

So what did the literature do? Country-pairs that saw expanded trade but weren’t in the enemy-ally classification got a new name: “connector countries.” This new ad hoc category helped make the 2025 pattern look like geopolitical fragmentation with a twist, rather than a mis-specified model.

My view is it is just simpler to think of the 2025 shift as a rerouting, not a realignment.

Summary and concluding remarks.

So is the world trade pattern fragmenting? Maybe that’s a tendency but I don’t think it is the more parsimonious explanation for what happened in 2025.

If the trading system were splitting into hostile blocs, like it did in the 1930s, we should have seen falling global openness. But in fact, the world on average became more open in 2025.

We should have seen a generalised drop in imports. But in fact, only 9 of the 108 nations that the WTO tracks saw their imports fall in 2025.[6]

If the US were cutting itself off from its geopolitical enemies, as defined by those with whom it has a trade deficit, its trade deficit should have shrunk. But in fact, it hit an all-time high.

If the world were breaking up into blocs, we might expect China’s goods exports to be harmed as its geopolitical enemies closed off their markets. But in fact, China’s exports hit a record in 2025 even as its direct sales to America fell.

Of course, the US tariff walls and Chinese export controls are real, but in 2025 they didn’t lead to global trade fragmentation.

The 2025 realised flows show that the weaponisation was mostly unilateral. Tariff aggression by the largest importer did not lead to system-wide escalation. It led to rerouting.

And that’s it for another Factful Friday!

References.

Bailey, M. A., Strezhnev, A., & Voeten, E. (2017). Estimating dynamic state preferences from United Nations voting data. Journal of Conflict Resolution, 61(2), 430–456.

Baldwin, R. (2026). World War Trade: Conflict, containment, and the emergent world trading order. CEPR Press.

Baldwin, R. (2026, May 15). Did Trumpian tariffs fragment America or the world trade system? Factful Friday, LinkedIn.

Carroll, L. (1872). Through the looking-glass, and what Alice found there. Macmillan.

Gopinath, G., Gourinchas, P.-O., Presbitero, A. F., & Topalova, P. (2025). Changing global linkages: A new Cold War? Journal of International Economics, 153, Article 104042.

McKinsey Global Institute. (2026). Geopolitics and the geometry of global trade: 2026 update. McKinsey & Company.

Qiu, H., Xia, D., & Yetman, J. (2024). Deconstructing global trade: The role of geopolitical alignment. BIS Quarterly Review, September, 35–47. https://www.bis.org/publ/qtrpdf/r_qt2409c.htm

UNCTAD. (2026). Global trade update (December 2025–April 2026 editions). United Nations Conference on Trade and Development.

[1] Gopinath, Gourinchas, Presbitero and Topalova (2025); McKinsey Global Institute (2026); UNCTAD (2026). Full details in the References.

[2] Baldwin (2026), World War Trade: Conflict, Containment, and the Emergent World Trading Order, CEPR Press.

[3] Matrix construction: six economies (US, Japan, Korea, China, extra-EU, Rest of World), merchandise trade, current US$. Each flow is valued by the destination’s reported imports (UN Comtrade), with exporter-reported mirror data and WTO totals used to fill gaps (notably China’s 2025 cells). RoW-to-RoW is a residual on an extra-EU basis.

[4] Bailey, Strezhnev and Voeten (2017), Journal of Conflict Resolution 61(2).

[5] Qiu, Xia and Yetman (2024), ‘Deconstructing global trade: The role of geopolitical alignment’, BIS Quarterly Review, September, pp. 35–47.

[6] See my Factful Friday of 15 May 2026, ‘Did Trumpian Tariffs Fragment America or the World Trade System?’, for the openness and import numbers; underlying data from the WTO and UNCTAD’s Global Trade Update.

Globalization is not disappearing. It is rerouting.

But focusing only on trade flows misses a deeper transformation.

While goods continue to move across borders, the institutions governing globalization are becoming increasingly fragmented. Export controls, investment screening, technology restrictions, sanctions, industrial policy, subsidy races, financial weaponization, and competing regulatory systems are creating a new landscape of economic security competition.

The physical movement of goods remains global. The rules, standards, and political foundations behind those flows are becoming more divided.

This is why the world today does not look like the deglobalization many predicted. Nor does it resemble the hyper-globalization of the 1990s and 2000s.

We are entering a new phase: a world of integrated production networks operating inside a progressively fragmented geopolitical order.

Understanding this distinction may be one of the most important challenges for interpreting the global economy in the decade ahead.